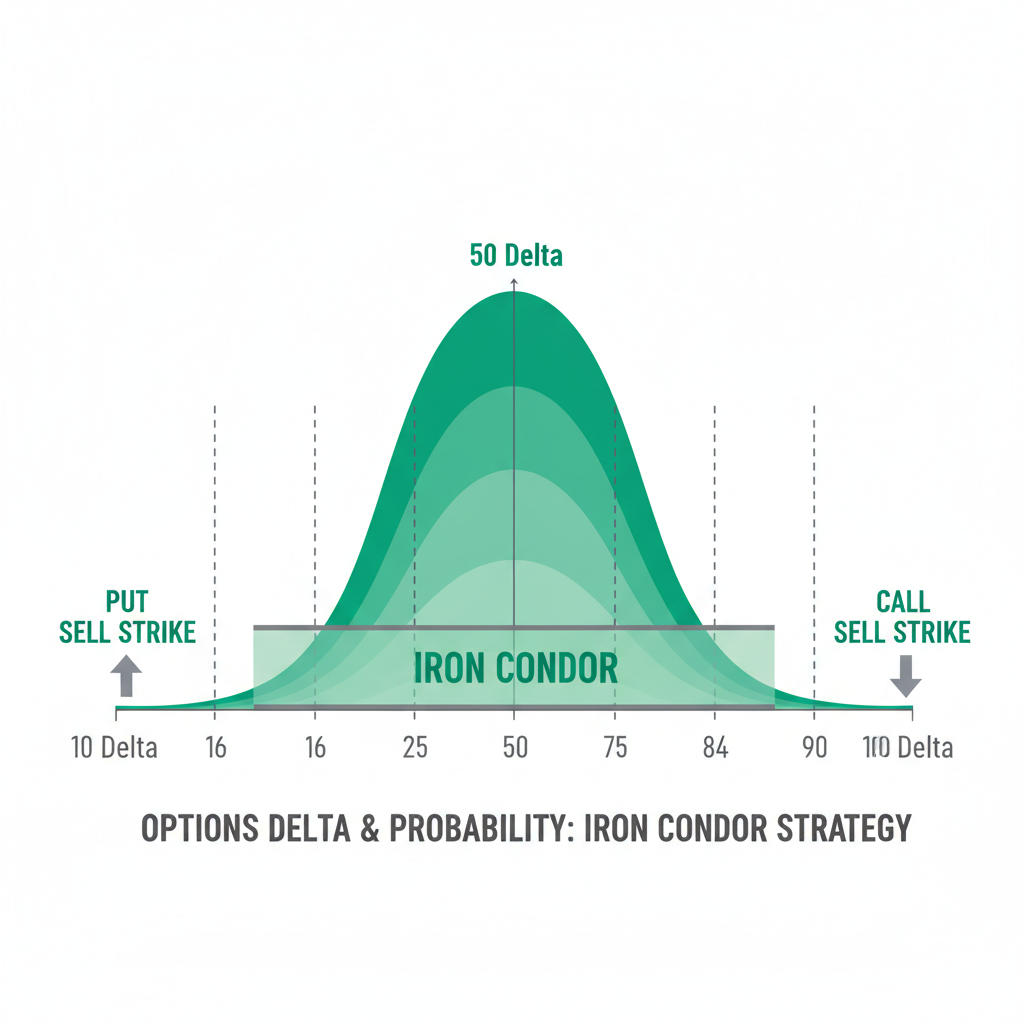

Delta Selection for Iron Condors: The Science Behind Strike Placement

The delta of your short strikes determines your probability of profit, your premium collected, and your risk. We ran the numbers on thousands of trades to find the optimal delta for each market regime.

Get Daily Iron Condor Picks

Unlock the automated screener, daily trade alerts, and the full research archive. Cancel anytime.

Share this article

Help others discover the Iron Condor Scalper — every share reaches a new potential investor.

Sharing with #IronCondorScalper helps us reach more options traders.

YOU MIGHT ALSO LIKE

The AI Tide: A Rising Sea or a Fleeting Wave?

The S&P 500 recently soared past the <strong>5,400</strong> mark, largely fueled by the relentless march of te…

Read articleThe Long & Short of It: Navigating the AI Gold Rush

The market saw a mixed bag this week, with the <strong>S&P 500</strong> inching up by <strong>0.5%</strong>, d…

Read articleThe Quiet Revolution: Value's Return Amidst AI's Roar

The S&P 500 closed up **0.75%** today, buoyed by a surprising resurgence in 'boring' sectors. Meanwhile, the N…

Read articleDiscussion

Sign in to join the discussion

No comments yet. Be the first to share your thoughts!